The Risk-Free Baseline: Why Your Bot Needs to Beat 5%

By Tommy Tietze, CEO of ArrowTrade AG

In retail algorithmic trading, there is a dangerous misconception that any profit is a good profit.

A trader builds a systematic bot, runs it for twelve months, and generates a 4% net return. They look at their equity curve, see that it goes up from left to right, and consider the project a success. After all, they beat the bank savings account, and they didn't lose money.

From a professional quantitative perspective, this trader did not make money. They lost money, and they took on massive structural risk to do so.

They failed to account for the most fundamental benchmark in finance: the risk-free rate. If your trading algorithm cannot significantly outperform the baseline yield of holding stablecoins, your algorithm has no mathematical justification to exist.

This article explains the concept of the risk-free baseline, why "Alpha" is the only metric that matters, and how to properly benchmark your automated system's actual performance.

Defining the Risk-Free Rate

In traditional finance, the risk-free rate is typically defined by the yield of short-term US Treasury bills. It represents the baseline return an investor can achieve with absolutely zero market risk.

In the cryptocurrency ecosystem, the equivalent is the stablecoin yield. If you hold USDT, USDC, or FDUSD on a major exchange like Binance and allocate it to a flexible "Earn" program, you are generally paid an annualized yield of roughly 4% to 6%. This yield is generated by the exchange utilizing your capital for over-collateralized margin lending.

You do not have to predict market direction. You do not have to write a single line of code. You do not suffer from slippage, trading fees, or stop-loss executions. You simply hold the digital equivalent of cash, and you are paid a continuous, compounding 5%.

This 5% is your baseline. It is the absolute minimum hurdle rate your algorithm must clear before it can claim to be profitable.

Alpha vs. Beta: The True Cost of Risk

When you turn your trading bot on, you instantly expose your capital to a cascade of risks:

- Market Risk: The asset you buy might crash.

- Execution Risk: The exchange API might fail, or you might suffer severe negative slippage during a volatile spike.

- Infrastructure Risk: Your server might crash, or your webhook might delay.

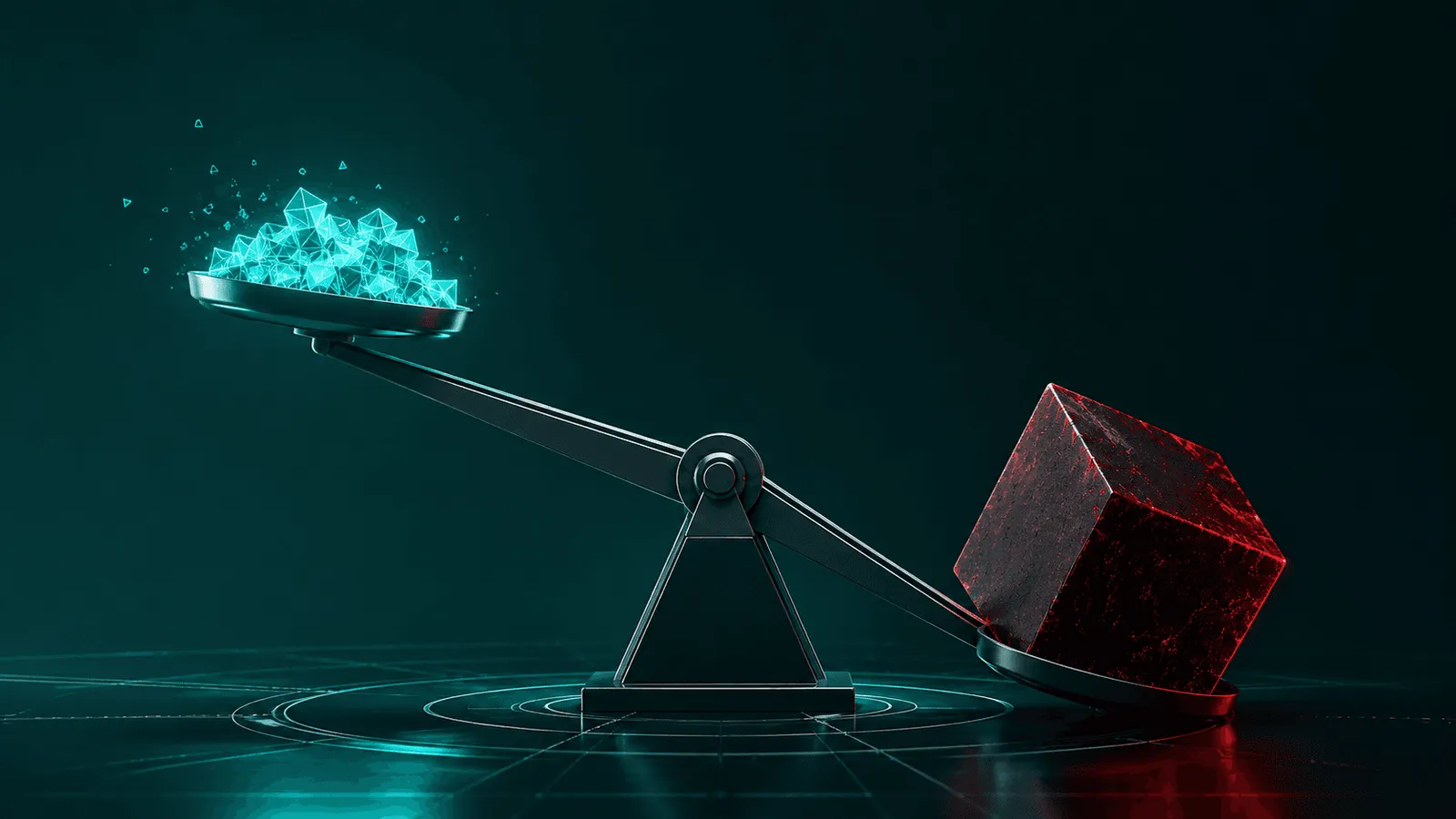

If your trading bot generates a 7% return over the year, you did not make 7% for taking on these risks. Because you could have made 5% by doing absolutely nothing, your algorithm only generated an excess return of 2%.

In quantitative finance, this excess return is called Alpha.

Taking on the extreme volatility, structural complexity, and fee drag of active algorithmic trading for a 2% Alpha is a terrible mathematical proposition. The risk-adjusted return is negative. You are picking up pennies in front of a steamroller.

Opportunity Cost and Dead Capital

Understanding the risk-free baseline completely changes how you view your portfolio during flat or sideways markets.

Many algorithmic traders design systems that sit in "cash" (stablecoins) for weeks, waiting for the perfect macro entry signal. This is structurally safe, but if that cash is sitting in an inactive spot wallet instead of a flexible yield account, it is suffering from opportunity cost.

A professional execution pipeline maximizes capital efficiency. When the bot is not actively deployed in a volatile asset, the capital should be working at the risk-free baseline. The moment the algorithm triggers a buy signal, the required capital is instantly redeemed from the flexible yield account and deployed into the spot market.

Setting the Institutional Benchmark

At unCoded, we advocate for ruthless, objective system analysis.

When you backtest or forward-test your execution logic, you must deduct the risk-free rate from your final equity curve. If your bot backtests at 12% Annualized Return, your actual Alpha is 7%. You then have to ask yourself: Does a 7% premium justify the Maximum Drawdown (MDD) the system experienced to achieve it?

If your system's Maximum Drawdown is 25%, and your generated Alpha is only 7%, your risk-to-reward architecture is fundamentally flawed. You are risking massive capital destruction for a marginal premium over the baseline.

A serious automated portfolio must aim for returns that mathematically compensate for the inherent danger of the crypto market. If it cannot, the smartest algorithmic decision you can make is to turn the bot off, park your capital in stablecoins, and collect your 5%.

Practical Checklist

The Risk-Free Audit for System Architects:

- Have you checked the current flexible Earn yield for your chosen stablecoin (USDT/USDC/FDUSD) on Binance?

- Does your algorithm's backtested annualized return significantly exceed this stablecoin baseline?

- Are you accurately calculating your system's "Alpha" (Total Bot Return minus the Risk-Free Rate)?

- When your bot sits in a 100% stablecoin position, is that capital sitting idle, or is it generating flexible yield?

- Does the excess return (Alpha) of your bot mathematically justify the maximum drawdown your capital is exposed to?

FAQ

What is a risk-free rate in crypto? It is the annualized percentage yield you can earn by holding stablecoins (like USDC or USDT) in low-risk, flexible savings or earn programs on tier-1 exchanges, without taking on any directional market exposure.

Why is a 4% bot return considered a loss? If the risk-free stablecoin yield is 5%, a bot that generates 4% has underperformed the baseline. You took on all the risk of active trading but made less money than if you had simply parked your cash and done nothing.

What is Alpha in algorithmic trading? Alpha is the excess return of your trading strategy compared to the baseline benchmark. If your bot makes 15% and the stablecoin yield is 5%, your Alpha is 10%.

Can unCoded trade with funds currently in Binance Earn? Binance allows automated spot trading utilizing funds that are held in specific Flexible Simple Earn products. A well-designed system accounts for available balance across both the spot wallet and flexible earn wallets to maximize capital efficiency.

Conclusion

Building a trading bot is easy. Building a trading bot that actually justifies its own existence is incredibly difficult.

The market does not owe you a premium just because you wrote a complex script. If you want to outperform the baseline, you must find a genuine mathematical edge, minimize your execution drag, and respect the cost of capital.

Serious Crypto means holding your algorithms to institutional standards. Stop celebrating returns that fail to beat the baseline. Measure your Alpha, optimize your capital velocity, and demand that your machine earns its keep.

Disclaimer: This article is for educational purposes only and is not financial advice. "Risk-free" refers to the absence of directional market risk; platform, counterparty, and smart contract risks still apply when holding stablecoins on any exchange. Cryptocurrency trading involves substantial risk.

Deploy institutional-grade execution infrastructure: unCoded

Engineered by: ArrowTrade AG

Recommended Reading

Portfolio Heat & Correlation: The Illusion of Diversification

By Tommy Tietze, CEO of ArrowTrade AG There is a fundamental misunderstanding in retail crypto tradi...

The Win Rate Illusion in Crypto Bots

By Tommy Tietze, CEO of ArrowTrade AG If you look at the marketing pages of retail crypto bots, you ...

Order Types in Crypto Trading

By Tommy Tietze, CEO of ArrowTrade AG Most traders spend weeks thinking about what to buy. Then they...

USDT, USDC and FDUSD Explained

By Tommy Tietze, CEO of ArrowTrade AG Stablecoins are often treated as if they were simply “digital ...